Private Equity

Harnessing the Growth of Private Markets

Summary

- Private equity funds offer traditional public equity market investors a means to dramatically expand their investment opportunity set and the potential to boost the growth profile of their portfolios.

- These funds are, however, far less liquid than traditional mutual funds and ETFs. The process to acquire, improve, and exit private companies takes time, and these businesses do not trade publicly. To capture the benefits, investors need a long-time horizon.

- Although there is a broad range of managers and strategies available, investors may face challenges accessing and evaluating the best options to meet their needs. Working with a scaled global asset manager that has institutional experience in these fields can help investors build a high-quality private equity allocation with institutional caliber governance and oversight.

Expanding investment opportunities

Private equity funds offer traditional public equity market investors a means to significantly expand their investment opportunity set and boost the growth profile of their portfolios.

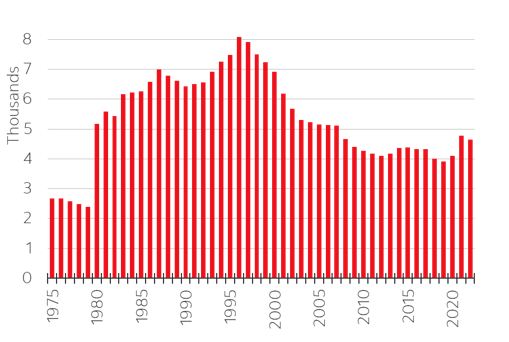

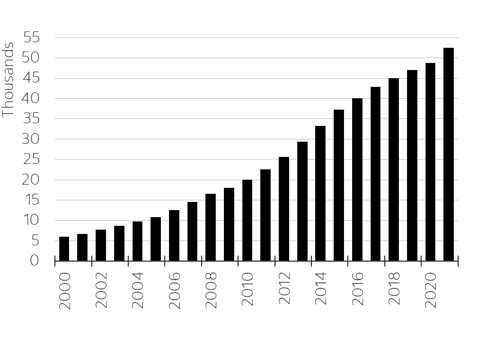

Investing in private equity has grown in relevance over the past couple of decades as the public markets have become more concentrated and as the total number of listed companies in the US has come down by approximately 40% (Fig. 1 LHS). Meanwhile, the number of companies held within private equity funds in the US has increased ten-fold and now outnumber public companies by nearly 10 to 1 (Fig. 1 RHS).

Figure 1. LHS: Number of U.S. listed companies, RHS: Number of private equity owned companies

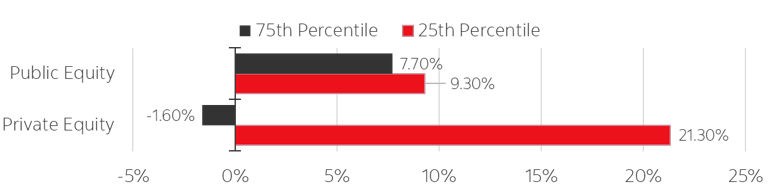

The demand for private equity capital solutions has grown from businesses who prefer to remain private, and work with a smaller number of active shareholders. The supply of capital from private equity investors (initially from large institutions and now from individual investors) has also increased to meet this demand, in large part encouraged by the attractive returns the private markets have provided (Fig. 2).

Figure 2. Price volatility and return statistics

Private equity funds pool investor capital into strategies that acquire, improve, and sell private companies in the pursuit of capital gains. Historically, private equity funds have on average outperformed public equities by more than 5% with less price volatility. Private equity is typically a high growth investment that generally does not distribute regular income.

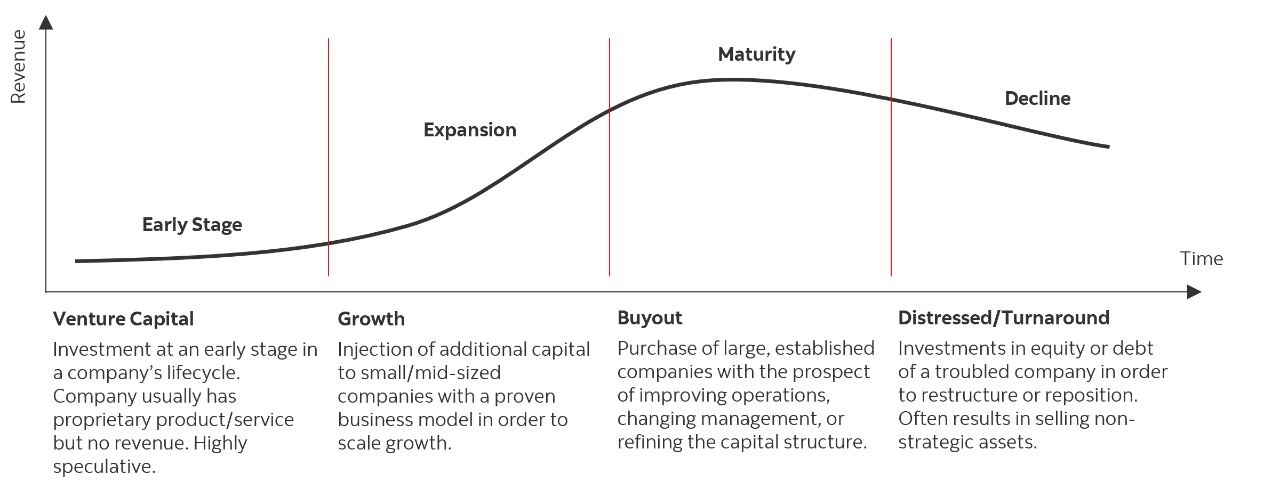

The higher returns versus public equity strategies are attributable to the much larger opportunity set that private equity managers have to work with (Fig. 3), the market inefficiencies and informational advantages that private investors can exploit, and the numerous ways to add value to, or even completely transform, a company as an active majority owner. These companies are also often at an earlier stage in their development relative to those that have undergone the IPO process and therefore have more room for earnings growth. Private businesses operating in rapidly growing parts of the market, like technology and healthcare, may have particularly long runways of growth potential ahead of them.

Figure 3. Opportunity set of public vs. private companies

The methodologies used to value private assets are generally less susceptible to short term swings in market sentiment that can drive higher price volatility in publicly traded assets. Private assets are valued much less frequently than their public equivalents, and often with a considerable lag.

Fundamental differences in the investment process combined with longer time horizons required to harvest the benefits of private market investments are all factors that contribute to an “illiquidity premium” investors in these strategies have generally earned in the past and continue to expect in the future.

This publication has been prepared by The Bank of Nova Scotia for Scotia Wealth Management clients. It is for general information purposes only and should not be considered or relied upon as personal and/or specific financial, tax, pension, insurance, legal or investment advice. We are not tax or legal advisors, and we recommend that individuals consult with their qualified advisors, including tax and legal advisors, before taking any action based upon the information contained in this publication. The opinions and projections contained in this publication are our own as of the date hereof and are subject to change without notice. Scotia Wealth Management is under no obligation to update this publication and readers should assume the information contained herein will not be updated. While care and attention has been taken to ensure the accuracy and reliability of the material in this publication, neither The Bank of Nova Scotia nor any of its affiliates or any of their respective directors, officers or employees make any representations or warranties, express or implied, as to the accuracy or completeness of such material and disclaim any liability resulting from any direct or consequential loss arising from any use of this publication or the information contained herein. This publication may contain forward-looking statements based on current expectations and projections about future general economic factors. Forward-looking statements are subject to inherent risks and uncertainties which may be unforeseeable and such expectations and projections may be incorrect in the future. Forward-looking statements are not guarantees of future performance and you should avoid placing undue reliance upon them. This publication and all the information, opinions and conclusions contained herein are protected by copyright. This publication may not be reproduced in whole or in part without the prior express consent of The Bank of Nova Scotia.

Scotia Wealth Management® in Canada consists of a range of financial services provided by The Bank of Nova Scotia (Scotiabank®); The Bank of Nova Scotia Trust Company (Scotiatrust®); Private Investment Counsel, a service of 1832 Asset Management L.P.; 1832 Asset Management U.S. Inc.; Scotia Wealth Insurance Services Inc.; and ScotiaMcLeod®, a division of Scotia Capital Inc. Private banking services are provided by Scotiabank. Estate and trust services are provided by The Bank of Nova Scotia Trust Company. Portfolio management is provided by 1832 Asset Management L.P. and 1832 Asset Management U.S. Inc. Insurance services are provided by Scotia Wealth Insurance Services Inc. Wealth advisory and brokerage services are provided by ScotiaMcLeod, a division of Scotia Capital Inc. International investment advisory services are provided by Scotia Capital Inc. Financial planning services are provided by Scotiabank and ScotiaMcLeod. Scotia Capital Inc. is a member of the Canadian Investor Protection Fund and regulated by the Canadian Investment Regulatory Organization. Scotia Wealth Insurance Services Inc. is the insurance subsidiary of Scotia Capital Inc., a member of the Scotiabank group of companies. When discussing life insurance products, ScotiaMcLeod advisors are acting as Life Insurance Agents (Financial Security Advisors in Quebec) representing Scotia Wealth Insurance Services Inc.

Scotia Wealth Management® is a Registered trademark of The Bank of Nova Scotia, used under licence.

© Copyright 2025 The Bank of Nova Scotia. All rights reserved.