Private Real Estate

Income and Growth from Real Assets

Summary

- Private real estate funds offer income and growth seeking investors a means to dramatically expand their investment opportunity set and build more stability and inflation resilience into their portfolios.

- These funds are, however, far less liquid than traditional mutual funds and ETFs. The process to acquire, improve, and exit commercial scale real estate properties takes time and these funds are not publicly traded. To capture the benefits, investors need a long-time horizon.

- Although there is a broad range of managers and strategies available, investors may face challenges accessing and evaluating the best options to meet their needs. Working with a scaled global asset manager that has institutional experience in these fields can help investors build a high-quality private real estate allocation with institutional caliber governance and oversight.

- Generating stable, inflation protected income

- Longer time horizon

- Established Private Real Estate Managers

Generating stable, inflation protected income

Private real estate funds offer income and growth seeking investors a means to dramatically expand their investment opportunity set and build more stability and inflation resilience into their portfolios.

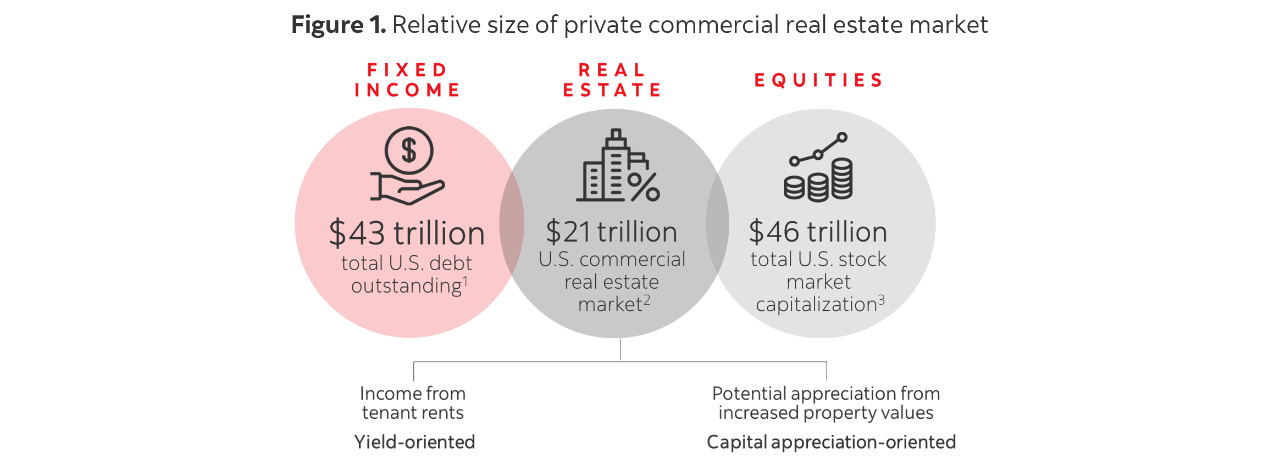

The commercial real estate market is broad and deep. With $21 trillion in market value in the US, it is about half the size of the US stock market in terms of market capitalization (Fig. 1). This market touches numerous areas that are generally grouped into residential, commercial, and industrial sub sectors. Investors can access these properties through the private markets, or through publicly traded real estate investment trusts (REITs).

2. Nareit, June 2021.

3. SIFMA, December 2023.

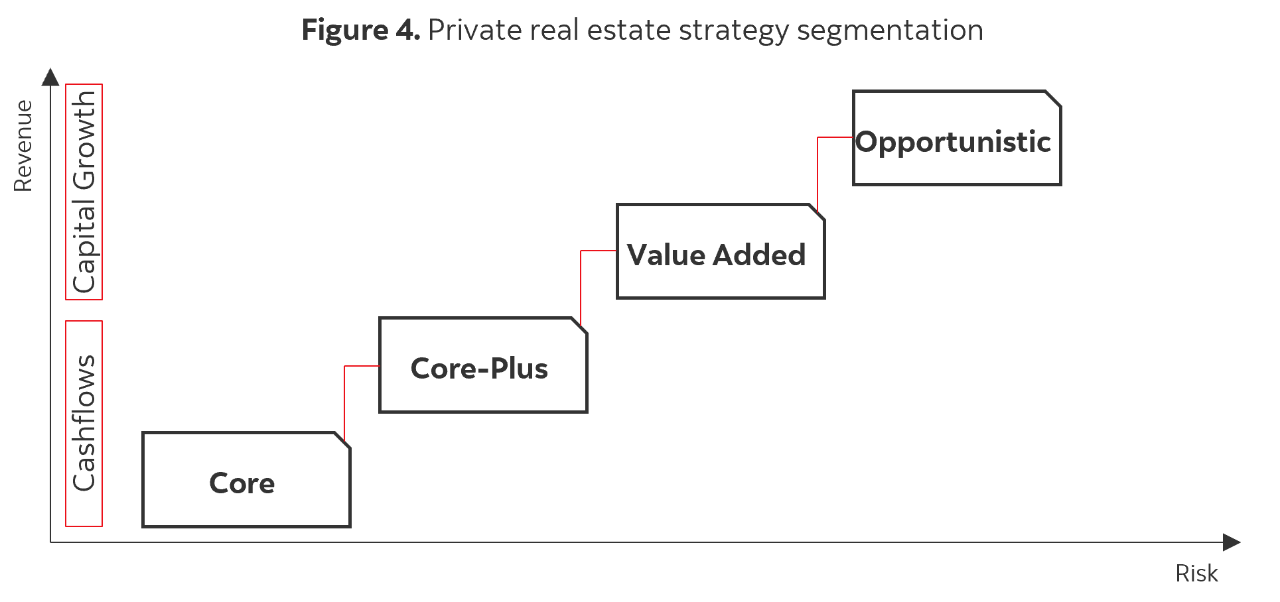

Real estate funds pool investor capital into strategies that acquire land and buildings with the intention to lease space in exchange for rental income, and/or generate capital gains through new development projects or building improvements.

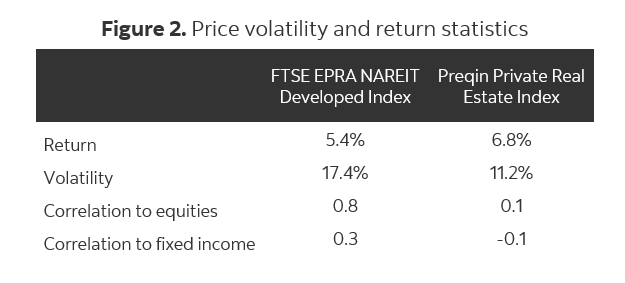

Private real estate is an equity investment, but the contractual nature of rental income generally makes the earnings profile less volatile than other more discretionary sectors of the market. These funds typically pay regular distributions that account for a significant piece of the total return. They have also outperformed public REITs by 1.4% with less volatility and with a much lower correlation to traditional stock and bond investments (Fig. 2).

The methodology used to value private real estate is less susceptible to short term swings in market sentiment that drives higher price volatility in publicly traded REITs and other listed equities. This may be a sought-after benefit that can contribute to portfolio stability.

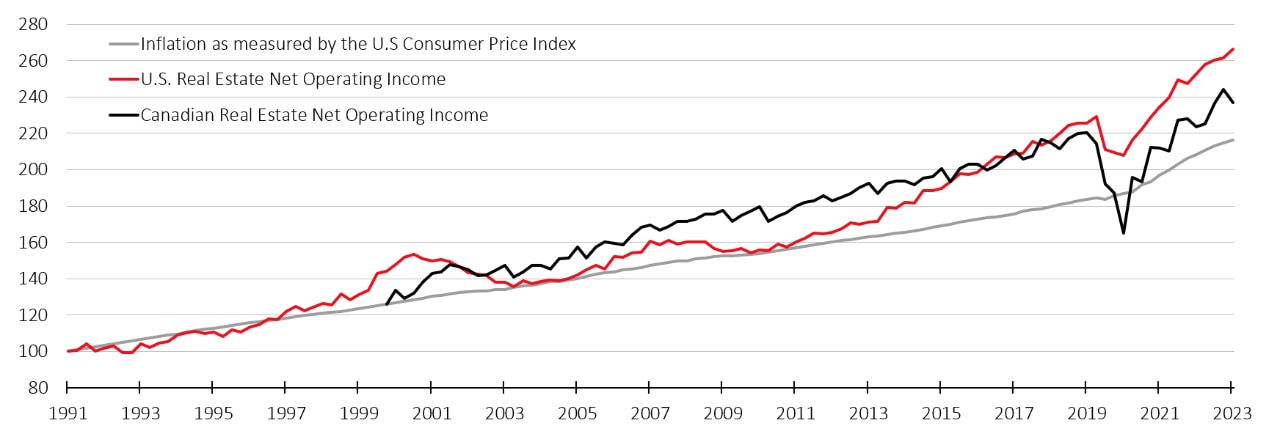

Rents and property values typically rise in tandem with inflation (Fig. 3), making private real estate a worthwhile tool to manage inflation risk in a portfolio. This is because higher construction costs result in higher replacement costs, which typically lead to higher rents due to limited supply, as higher construction costs discourage new developments. This scarcity often enables building owners to charge more, particularly when new or renovated properties have higher market comparables. Furthermore, lease structures frequently include periodic rent increases, as well as the ability to pass on rising operating costs to tenants, both of which help to protect the real, inflation adjusted income and growth stream they can provide to investors.

Figure 3. Inflation protected income and growth stream

Scotia Global Asset Management® is a provider of global investment management solutions and is a registered trademark of The Bank of Nova Scotia, used under license. Scotia Global Asset Management includes the following subsidiaries of The Bank of Nova Scotia: 1832 Asset Management L.P. (Canada), Scotia Administradora General de Fondos Chile S.A (Chile), Scotia Fondos Sociedad Administradora de Fondos Mutuos S.A. (Peru), Scotia Fondos S.A. de C.V. (Mexico), Sociedad Operadora de Fondos de Inversión Grupo Financiero Scotiabank Inverlat (Mexico), Scotiabank & Trust (Cayman) Ltd. (Cayman Islands), and Scotia Investments Jamaica Limited (Jamaica).

Scotia Global Asset Management’s broad range of investment management solutions are also made available through its affiliates and distribution partners. These include: Jarislowsky, Fraser Limited, MD Financial Management Inc. and MD Management Limited, Tangerine Investment Funds Limited, Private Investment Counsel, a service of 1832 Asset Management L.P., Scotia Capital Inc., Scotia Securities Inc., Scotiabank Inverlat, S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Scotiabank Chile S.A., Scotia Administradora General de Fondos Chile S.A, The Bank of Nova Scotia Jamaica Limited, Scotiabank & Trust (Cayman) Ltd and other affiliates of The Bank of Nova Scotia.

This publication has been prepared by Scotia Global Asset Management. It is for general information purposes only and should not be considered or relied upon as personal and/or specific financial, tax, pension, insurance, legal or investment advice. We are not tax or legal advisors, and we recommend that individuals consult with their qualified advisors, including tax and legal advisors, before taking any action based upon the information contained in this publication. The opinions and projections contained in this publication are our own as of the date hereof and are subject to change without notice. Scotia Wealth Management is under no obligation to update this publication and readers should assume the information contained herein will not be updated. While care and attention has been taken to ensure the accuracy and reliability of the material in this publication, neither The Bank of Nova Scotia nor any of its affiliates or any of their respective directors, officers or employees make any representations or warranties, express or implied, as to the accuracy or completeness of such material and disclaim any liability resulting from any direct or consequential loss arising from any use of this publication or the information contained herein. This publication may contain forward-looking statements based on current expectations and projections about future general economic factors. Forward-looking statements are subject to inherent risks and uncertainties which may be unforeseeable and such expectations and projections may be incorrect in the future. Forward-looking statements are not guarantees of future performance and you should avoid placing undue reliance upon them. This publication and all the information, opinions and conclusions contained herein are protected by copyright. This publication may not be reproduced in whole or in part without the prior express consent of The Bank of Nova Scotia.

© Copyright 2025 The Bank of Nova Scotia. All rights reserved.